22:00 Beijing time tonight Global markets will be focused on a seemingly dry piece of data released by the U.S. Bureau of Labor Statistics: the revised preliminary estimate of non-farm payrolls for 2025. However, this is no ordinary monthly jobs report, but rather the ultimate "fact check" on the myths surrounding the U.S. economy over the past year. With market expectations of 800,000 inaccuracies being squeezed out, how could this statistical "anti-counterfeiting storm" potentially become leverage for the Federal Reserve to aggressively cut interest rates and unleash a massive wave of volatility in the crypto world?

In the cryptocurrency world, we're accustomed to tracking on-chain data, focusing on technical narratives, and interpreting project white papers. But sometimes, market trends can be determined by a traditional-sounding economic indicator from the "old world" (TradFi). Tonight's non-farm payroll benchmark revision is just such a key factor.

It's not like the monthly non-farm payroll report, which simply tells us how good or bad the job market was last month. Instead, it's like a rigorous auditor looking back at the data for the past year and saying, "Hey, maybe we were wrong all along."

What exactly is being corrected? It’s not an update, it’s an error correction.

To understand the significance of this revision, we must first understand what it is revising.

The monthly non-farm payroll data (CES report) is essentially an estimate. It's derived from a sample survey of approximately 119,000 businesses, prioritizing timeliness at the expense of accuracy. To compensate for the sample limitations, the statistics agency also uses a "birth/death model" to estimate employment changes at newly established and closed companies.

The annual benchmark revision is calibrated using a more authoritative and comprehensive data set: the Quarterly Census of Employment and Wages (QCEW). The QCEW data covers 95% of jobs in the United States. Because it comes directly from state unemployment insurance tax records, it is almost equivalent to an employment "census."

Simply put, the monthly non-farm payroll report is like a quick poll, while the annual revision is the final tally.

The focus tonight is that the market generally predicts that the "vote count results" will be significantly lower than the previous "opinion polls." The downward revision of up to 800,000 expectations means that the "employment engine" of the US economy may not be as strong as we thought in the past year, and there may even be a considerable "bubble."

Why do we need to revise? When “estimates” fail to keep up with reality

The core reason for such a huge deviation in expectations is probably the "corporate life and death model".

This model works well during periods of economic stability. However, in the post-pandemic era of dramatic economic structural changes, especially in a high-interest environment, small businesses face increasing pressure to survive, and the wave of bankruptcies may far exceed the model's estimates. Every inaccuracy in the model means an overestimated employment report.

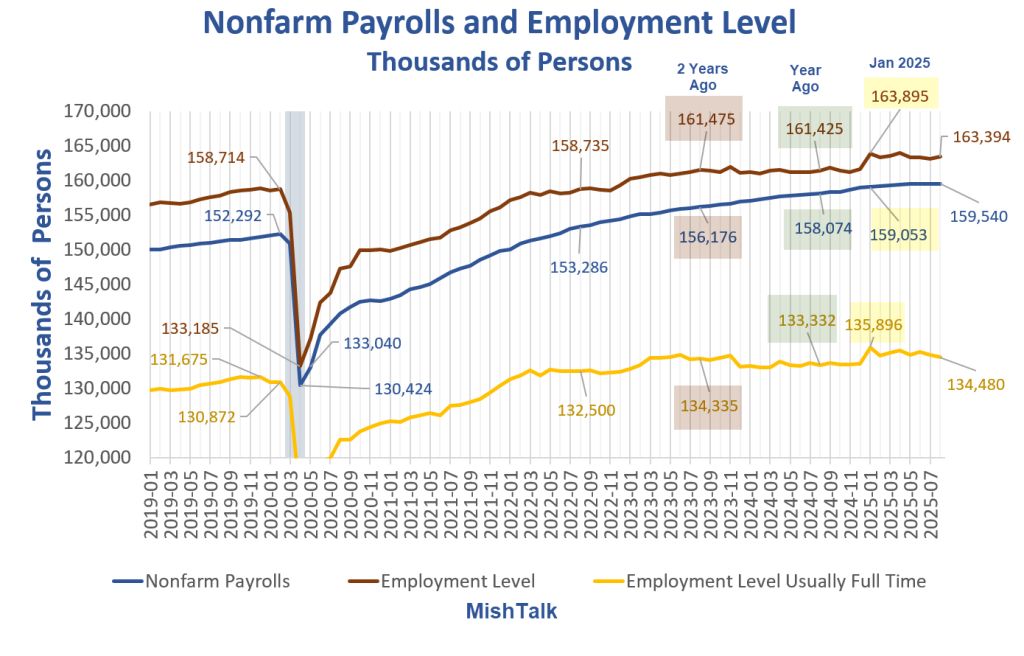

In fact, suspicions of overestimation in employment data are not unfounded. Different statistical calibers have long presented conflicting pictures. First, problems have long been apparent regarding the "quality" of employment. As shown in the figure below, while the "non-farm payroll" data (blue line), which represents overall employment growth, continues to climb, the "full-time employment level" (yellow line), which better reflects the health of the economy, has long stagnated. The widening gap between the two curves, forming the so-called "scissors gap" in the data, strongly suggests that the majority of new jobs may be part-time or temporary, and that the labor market is on shaky ground.

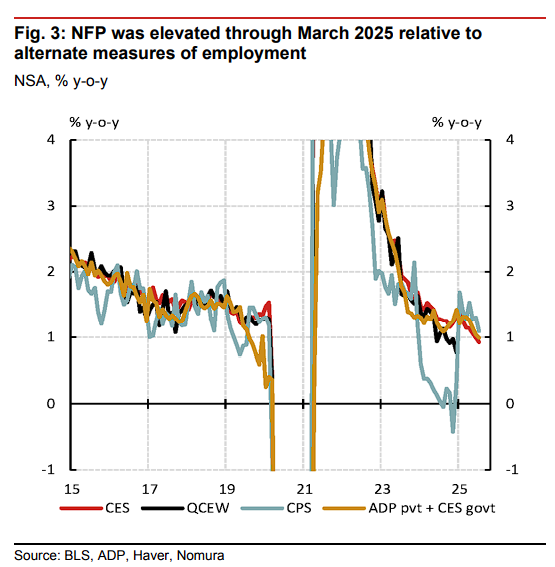

Secondly, the overestimation is even more evident when looking at employment statistics. The chart below directly compares the year-over-year growth rates of various employment data. Note the red line (CES, representing the monthly non-farm payroll estimate) and the black line (QCEW, representing the more accurate census). We can clearly see that since 2023, the red line has consistently run above the black line. This systematic deviation is the core reason for the market's prediction that this revision will significantly "drain the water." It practically declares that the "good news" we hear every month may be adulterated.

When the evidence of declining employment "quality" and overestimation of "quantity" is combined, a shocking truth may surface: the "strong job market" that has supported the Federal Reserve's hawkish stance and made the market confident of a "soft landing" in the past may just be a "mirage" beautified by statistical data.

Detonating the market: From “data falsification” to “policy shift”

If the "myth" of the job market is falsified, the dominoes will fall.

- The Federal Reserve's "Crisis of Faith": Over the past year, Fed Chairman Powell has cited a "strong labor market" as the core rationale for his decisions in nearly every press conference. If this rationale is proven false, the Fed's entire policy framework will face legitimacy doubts. Were their previous decisions based on "overheated" employment data wrong from the outset?

- The door is open to a 50 basis point rate cut: A much weaker-than-expected job market means the risk of a recession has risen sharply, while the inflationary wage spiral has weakened significantly. In this context, a mere 25 basis point rate cut may no longer be sufficient. To avoid a hard landing, a more decisive action—a 50 basis point rate cut—would move from a radical conjecture to a realistic option on the table.

- The “liquidity feast” of the crypto market: this is the part that is most relevant to us.

- Macroeconomic liquidity injection: Any unexpected interest rate cut, especially a 50 basis point cut, sends a clear easing signal to global markets. Once the floodgates of US dollar liquidity are opened, the crypto market, one of the most liquidity-sensitive asset classes, will undoubtedly see the most immediate boost. Historical cycles clearly show that the core fuel of crypto bull markets is always macroeconomic liquidity.

- The power of narrative: The market narrative will shift completely from "anti-inflation" to "recession-proofing." Amidst heightened economic uncertainty, Bitcoin's "digital gold" and store-of-value attributes will be re-emphasized. As the purchasing power of fiat currencies erodes due to loose monetary policy, the search for hard assets will become a consensus, and Bitcoin is one of the most unique hard assets of this era.

Conclusion: Fasten your seat belts for the “moment of truth”

Tonight's data revision is less an economic event and more of a "moment of truth" that will force markets to reassess the past and repricing the future.

For crypto investors, this isn't just another night of staying up late to watch the market. We need to understand that this correction means much more than just the numbers themselves. It holds a key that could unlock the Pandora's box of the Federal Reserve's monetary policy and ultimately determine whether the flow of funds into the crypto world will be a trickle or a torrent in the coming months and beyond.

Please closely monitor the market reaction following the data release, especially the dollar index, U.S. Treasury yields, and the associated performance of risky assets. Of course, be prepared for potential volatility. Because when the truth comes out, the market never calms down.