Author: Dio Casares

Translated by: TechFlow

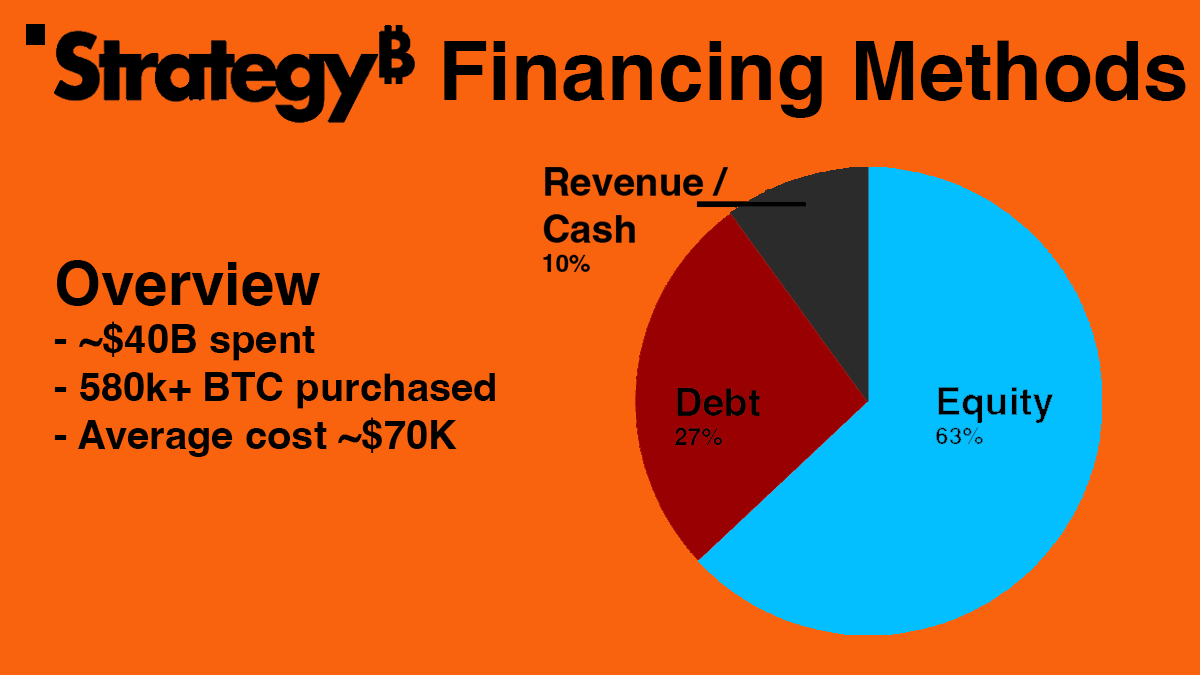

Over the past 5 years, Strategy has spent $40.8 billion, equivalent to Iceland's GDP, purchasing over 580,000 Bit. This represents 2.9% of the Bit supply or nearly 10% of active Bit (1).

Strategy's stock ticker $MSTR has risen 1600% in the past three years, compared to Bit's rise of only about 420%. This significant growth has pushed Strategy's valuation beyond $100 billion and led to its inclusion in the Nasdaq 100 index.

This massive growth has also raised doubts. Some claim $MSTR will become a trillion-dollar company, while others sound the alarm, questioning whether Strategy might be forced to sell its Bit, potentially triggering a massive panic that could suppress Bit prices for years.

However, while these concerns are not entirely unfounded, most people lack a basic understanding of Strategy's operations. This article will explore in detail how Strategy operates and whether it represents a major risk in Bit acquisition or a revolutionary model.

How Did Strategy Purchase So Much Bit?

Note: Data may differ from the time of writing due to new financing and other reasons.

Broadly speaking, Strategy primarily acquires funds to purchase Bit through three methods: revenue from its operational business, stock/equity sales, and debt. Among these three methods, debt is undoubtedly the most scrutinized. While people often focus heavily on debt, in reality, the vast majority of funds used by Strategy to purchase Bit comes from issuance, which means selling stocks to the public and using the proceeds to buy Bit.

This might seem counterintuitive - why would people buy Strategy's stock instead of directly purchasing Bit? The reason is simple, returning to the most beloved business type in the crypto field: arbitrage.

Why People Choose to Buy $MSTR Instead of Directly Buying $BTC

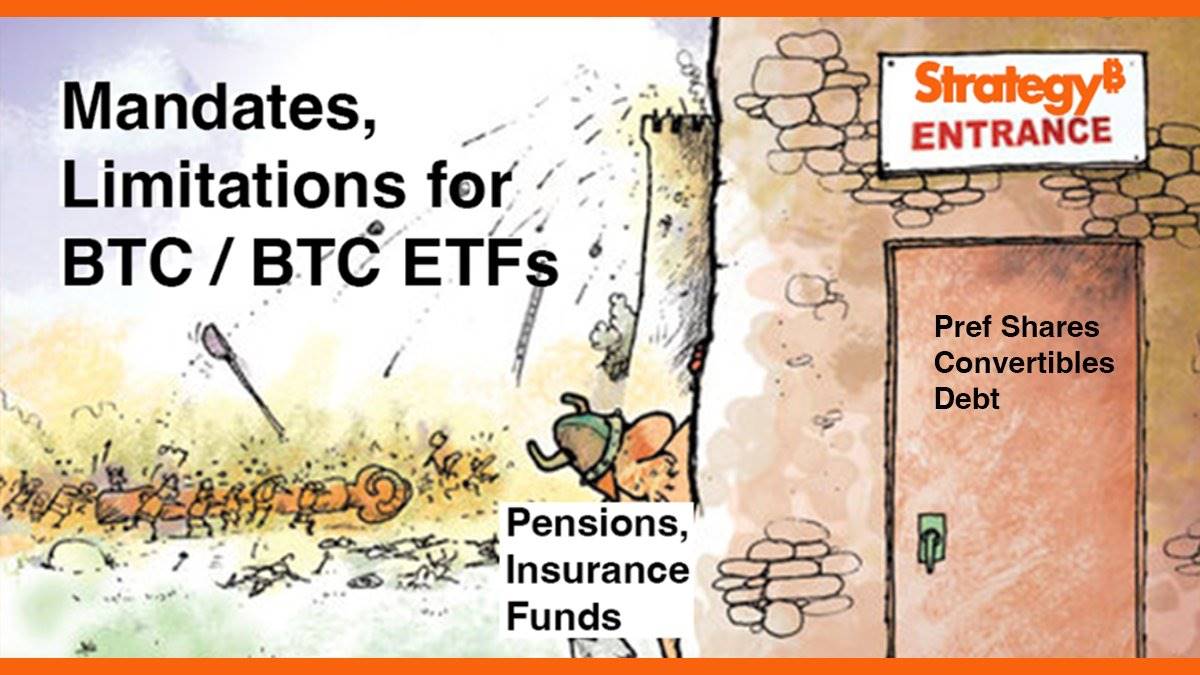

Many institutions, funds, and regulated entities are restricted by "investment mandates". These mandates specify which assets a company can and cannot purchase. For example, credit funds can only buy credit instruments, stock funds can only buy stocks, and long-only funds can never short, and so on.

These mandates allow investors to be confident that, for instance, a stock-only fund won't buy sovereign debt, and vice versa. They compel fund managers and regulated entities like banks and insurance companies to be more responsible, only taking on specific types of risks rather than being able to take on any type of risk. After all, the risk of buying Nvidia stock is entirely different from buying US Treasury bonds or investing in money market funds.

Due to these highly conservative mandates, much capital locked in funds and entities is "trapped", unable to enter emerging industries or opportunity areas, including cryptocurrencies, especially unable to directly touch Bit, even if the fund managers and related personnel wish to somehow access Bit.

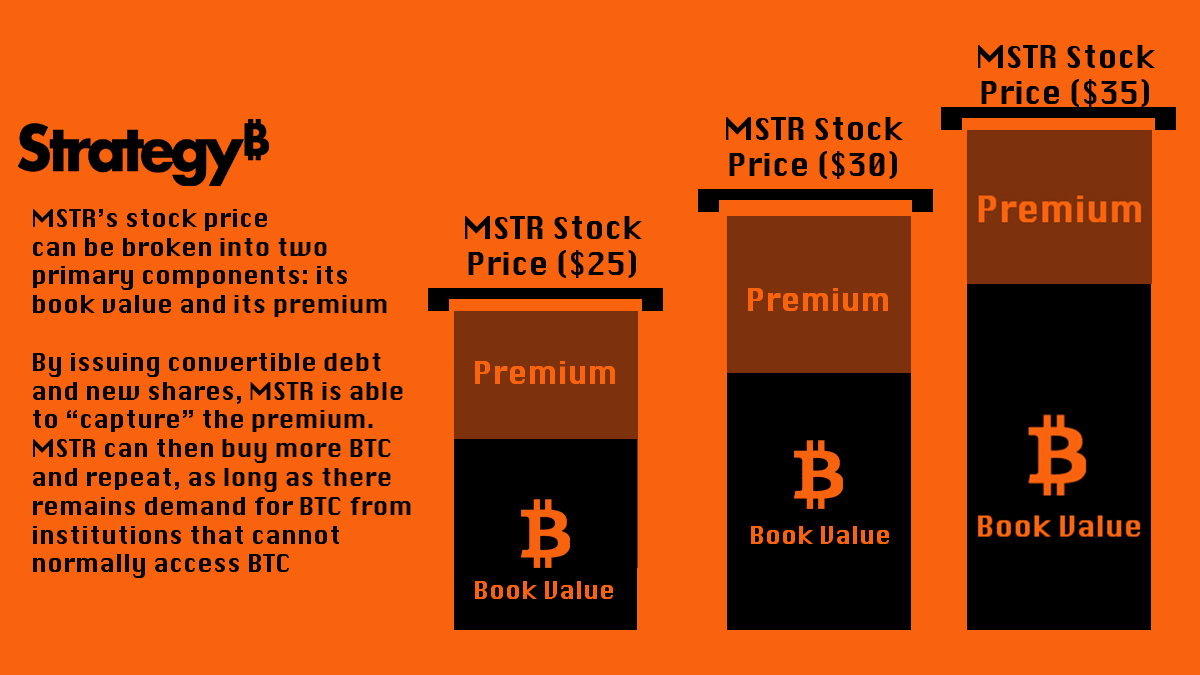

Strategy's founder and executive chairman Michael Saylor saw the difference between these entities' desire to gain asset exposure and the risks they can actually bear, and exploited this. Before Bit ETFs, $MSTR was one of the few reliable ways for entities that could only buy stocks to gain Bit exposure. This meant Strategy's stock often traded at a premium because demand for $MSTR exceeded its stock supply. Strategy continuously leveraged this premium - the difference between $MSTR stock value and the Bit value per share - to buy more Bit while increasing the Bit per share.

In the past two years, if you held $MSTR, your "returns" in Bit terms reached 134%, the highest scaled Bit investment return in the market. Strategy's product directly met the needs of entities that typically couldn't access Bit.

This is a typical case of "Mandate Arbitrage". Before Bit ETFs were launched, as mentioned earlier, many market participants couldn't buy non-exchange-traded stocks or securities. However, as a listed company, Strategy was allowed to hold and buy Bit ($BTC). Even with recent Bit ETF launches, believing this strategy is no longer effective is completely wrong, as many funds are still prohibited from investing in ETFs, including most mutual funds managing $25 trillion in assets.

A typical case study is Capital Group's Capital International Investors Fund (CII). The fund manages $509 billion in assets but is restricted to the stock domain, unable to directly hold commodities or ETFs (Bit is mostly viewed as a commodity in the US). Due to these restrictions, Strategy became one of the few tools CII could use to gain Bit price volatility exposure. In fact, CII's confidence in Strategy is so high that it holds about 12% of Strategy's stock, making CII one of the largest non-insider shareholders.

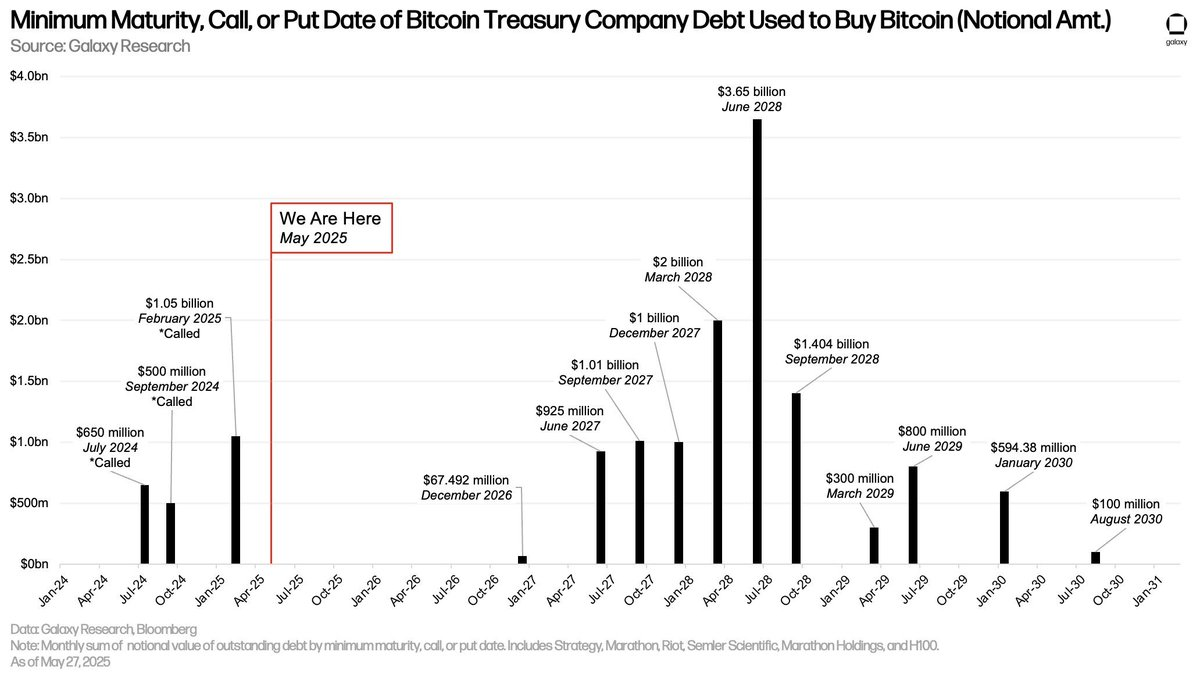

Debt Terms: A Constraint for Other Companies, But an Advantage for Strategy

Beyond the positive supply situation, Strategy also has certain advantages in the debt it takes on. Not all debt is the same. Credit card debt, mortgage loans, margin loans are entirely different types of debt.

Credit card debt is personal debt, dependent on your salary and ability to repay, unsupported by assets, and typically carrying annual interest rates of over 20%. Margin loans are typically issued against assets you already own (usually stocks), and if your total asset value approaches the amount you owe, your broker or bank might seize all your funds. Mortgage loans, however, are seen as the "holy grail" of debt, as they allow you to buy assets that typically appreciate (like houses) while only paying monthly loan interest (mortgage payments).

Although this is not entirely risk-free, especially in the current interest rate environment where interest can accumulate to unsustainable levels, it remains the most flexible compared to other loan types, with lower interest rates, and assets won't be seized as long as monthly payments are made on time.

Typically, mortgage loans are limited to housing. However, corporate loans can sometimes operate similarly to mortgages, meaning interest is paid within a specified time, and the principal (initial loan amount) only needs to be repaid at the end of that period. Although loan terms can vary significantly, generally, as long as interest is paid on time, debt holders have no right to sell the company's assets.

Chart source: @glxyresearch

This flexibility allows corporate borrowers like Strategy to more easily navigate market fluctuations, making $MSTR a way to "harvest" crypto market volatility. However, this does not mean risks are completely eliminated.

Conclusion

Strategy is not in the leveraged business, but in the arbitrage business.

Although currently holding a certain amount of debt, Bit prices would need to drop to around $15,000 per Bit within five years to pose a serious risk to Strategy. With the expansion of "treasury companies" (companies replicating Strategy's Bit accumulation strategy), including MetaPlanet, Nakamoto by @DavidFBailey, and others, this will become a focus of another topic.

However, if these treasury companies stop collecting premiums to compete with each other and start taking on excessive debt, the entire situation will change and could bring serious consequences.